How many times have you heard the words “customers don’t like to be pressured to buy”?

I’ve used those words myself many times when talking to dealers and manufacturers. But I’ve also had a long-standing, nagging scepticism that the research that this and other conclusions are based on has a built-in bias — the questionnaire itself.

Almost all consumer surveys that measure the new vehicle purchase experience include a question about whether or not the salesperson pressured the customer to buy (that day or generally). That’s fine, but perhaps the question guides many customers to provide a predictable response: “now that you mention it, yes there was pressure to buy.”

A different research approach might give a different (more accurate) answer

A new and different way of conducting research has emerged in the past few years — one that uses artificial intelligence (AI) to analyse consumer conversations on social media, providing new and unfiltered insight into what consumers think and do.

One company that does this is a start-up organization from Ottawa, Advanced Symbolics. Advanced Symbolics first made an impact in the political arena by very accurately predicting Trump’s win in 2016, the Brexit decision and the Liberal Party’s victory in the last federal election in Canada. These predictions were all at odds with those of traditional polling firms.

The company “listens” to consumer conversations on social media, applies a proprietary sampling algorithm to ensure that the sample is representative of the Canadian population and then applies AI algorithms to better understand consumer concerns and attitudes.

The key components for analysis are Engagement and Stance. The level of engagement tells us how many consumers are engaged in discussing a particular topic: is this an issue that defines consumers or influences their behaviour?

Stance tells us whether consumers are positive or negative on a topic, who is most positive or negative and helps prioritize actions or communication messages. A patented sampling methodology and the ability to predict consumer responses set Advanced Symbolics’ approach apart from most social media measurement approaches.

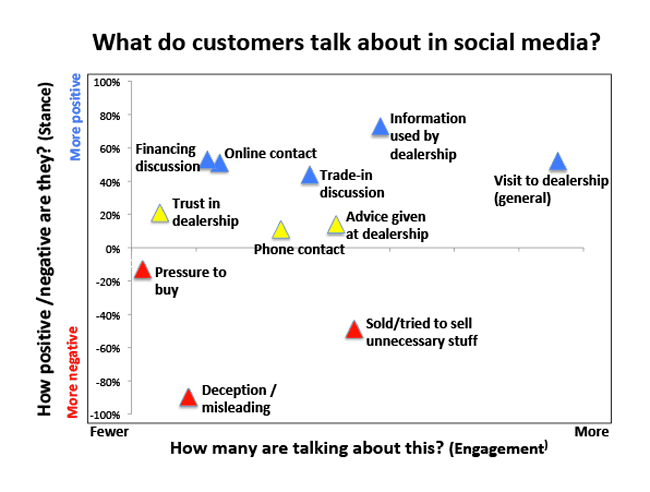

I recently worked with Advanced Symbolics on a project to better understand the dynamics of the consumer purchase funnel for new vehicles. The chart below shows how consumers (potential vehicle buyers) talked about these eleven different topics.

On the horizontal axis you can see the engagement level. If a topic is further to the right, it means that more consumers are discussing it.

On the vertical axis, the higher up a topic is, the more positively consumers talk about it.

The visit to the dealership in general is widely discussed — mostly in a positive way. The financing discussion is also mostly positive, but not something that consumers talk about that often.

On the negative side, upselling is the most widely discussed negative experience. Pressure to buy has very low engagement and although negative, it is not nearly as negative as when consumers feel deceived or misled.

Also interesting to note is that, while telephone contact with the dealership is mentioned more than on-line contact, the latter is more positively viewed.

Another area that stands out is the feeling of trust. Very few consumers talk about trust in the dealership.

This may be because trust is an outcome of many different factors and is a feeling not a specific event of the purchase experience.

But trust is clearly not top-of-mind with consumers or something that stands out enough for them to talk about it. Trust is hard to earn but very easy to lose. Any dealership that has customers or prospects that talk about trust in a positive way is likely to stand out from the crowd.

The visit to the dealership in general is widely discussed — mostly in a positive way. The financing discussion is also mostly positive, but not something that consumers talk about that often.

The purchase experience: positives and negatives

An overall observation is that, contrary to popular belief, customer interaction with dealerships is not all negative.

Take away the pre-designed questions about pressure to buy and discussion on trade-in and just listen to what customers and prospects say. Much of it is positive.

There are some negatives, however — the biggest of which is the practice of selling more than the customer asks for.

In many cases, this is likely done in a positive way (making the customer aware of options for upgrades, insurance, etc.), but it’s not necessarily seen as positive by the customer.

Perhaps there is a better way of integrating this into the sales process — one that feels less like a push for “add-ons.” That may be difficult when we still adhere to the Sales/Service/F&I silos.

Perhaps there is a better way of integrating this into the sales process — one that feels less like a push for “add-ons.”

How much of this will be relevant in a new retail world?

All this relates to a world in which the existing model of auto retailing prevails.

That’s pretty much all that consumers can comment on right now and they don’t seem to feel the need to express ideas about “the car-buying experience of the future.”

Consumers are largely feeling stuck with the status quo, but they will vote with their feet (and wallets) if anyone comes up with a new way of doing things that fits in with their dynamic needs. This has already happened in many other retail environments.

Boston Consulting Group (BCG) published a very interesting paper called “It’s time for a new way to sell cars” (October, 2018). We’ve all heard that so often in recent years, but radical change has not happened. BCG paints four likely scenarios for the future of auto retailing:

OEM Driven Sales

- Traditional players

- On-line only sellers

Digital-driven Third Party Sales

- e-Commerce aggregators (tech and e-commerce giants

- Third party multibrand sellers

Change might be evolutionary, moving first to on-line only sellers (Lynk & Co.) and then to the third-party sales scenarios, but it could also come suddenly if there is a catalyst in the form of Alibaba. Interesting that both of these examples mentioned by BCG have China roots.

But we live in the present and have to deal with the realities of the existing traditional model. So, pressure to buy and selling more than the customer wants are still part of the world of the dealership.

We just need to put things into perspective and listen more carefully to customers, without the filter of a survey.

There will always be a need for survey questions, but a better combination of listening and asking will give us new insights. Pair that with AI that can predict customer responses to actions or messages and we have a win.