In our first missive we sent out on the COVID-19 issue, we mentioned three big unknowns:

- How bad is it going to be

- How long will it last … and

- What will the ramp up period look like once this is over

After three weeks of a virtual shutdown of the economic system across Canada, we now know the answer to the first question. It is bad. Indeed very bad, especially for the automotive sector. There is no possible sugar coating for the severity of the problem. We still can’t answer the next two questions.

We would argue that the automotive sector has been one of the hardest hit in Canada. That is not to discount how much devastation has occurred in the entertainment industry, travel sector, restaurants, hotels, etc. They obviously are the most visible sectors affected and have been very hard hit, but there are some differences between them and the automotive sector.

First of all we know that the automotive sector directly employs between 700K and 800K employees in Canada, so it is very large. But some of these other sectors are also large.

Second, and this distinguishes automotive from most others, it is also is one of the best paid sectors in Canada. This means that the multiplier impact of the automotive sector is very high and possibly the highest of any other sector in Canada. It is absolutely true that one in seven jobs in Canada and one in six in Ontario are dependent directly and “indirectly” on the automotive sector. This is the multiplier effect.

The third issue is tougher to explain. The sector has about 200K workers on the manufacturing side of the sector, and about 500K to 600K workers on the non-manufacturing side. This includes retailing new and used vehicles, financing these vehicles, distribution of vehicles and aftermarket parts, repairing vehicles, and more. New car dealers alone employ more workers than the assembly and parts sector together. Same with the aftermarket.

To control the virus every level of government and virtually every business (other than some essential services) have asked their employees to stay home, to isolate themselves, cocoon, to adhere to social distancing guidelines — there are many names for it.

What this means in automotive “speak” is that consumers are NOT using their vehicles. The average Canadian drives about 25K kilometres a year. That translates into about 650 billion kilometres per year, or between 13-15 billion kilometres per week.

We don’t know for sure, but we estimate that somewhere between 65 per cent and 85 per cent of driving of light vehicles has disappeared because of the response to the pandemic. That translates into about at least 7 billion, and as much as 9 billion fewer kilometres driven per week.

Embedded into each vehicle bought in Canada is about 275,000 to 325,000 kilometres of expected useful life. So with all this lost driving we are essentially NOT using up the embedded kilometers of about 25,000 to 35,000 vehicles per week. That means we are not replacing them.

A lot of consumers stay out of the market during the end of the year and the winter months, so beginning in March we see a catch up for these consumers that increases sales in March to June (roughly 200K new per month) before the market stabilizes over the summer at about 180K new vehicles per month. So during these months (except March) you are likely to see 35,000 to 45,000 fewer new vehicle sales per week.

And most important, the current downturn is unlike a normal market cyclical correction for this industry. During the financial crisis, the Gulf War, the first oil embargo, etc., the sector went through a correction, but vehicle owners were still driving and using up the embedded kilometers in their vehicle.

This created millions of units of pent up demand that came forward after these crises abated. This will not happen during this crisis. Vehicles NOT bought the last few weeks and over the next month or two will not be picked up — ever. The market will not come back to some semblance of normalcy until consumers begin to drive their vehicles again. The most popular question I get is how long will this last…that is my answer.

We now know how deep — we just don’t know how long. So to simplify the question, I’ve boiled it down to a weekly analysis. If you think it will be 10 weeks, then take my 35-45K per week and multiply it by 10 and you will get a rough estimate of the impact. If you think it will be shorter or longer, then all one has to do is the math.

I haven’t done a similar analysis for the North American market, but I believe the numbers would hold. Canada is about 7-8 per cent of the North American market, so my Canadian number would translate into about 450,000 to 550,000 new vehicles lost per week on a North American basis. But don’t hold me to this number.

I want to get back to the two groups of workers. When usage of vehicles returns, the jobs in the non-manufacturing sector will return very quickly. But the U.S. governments (especially at the federal level) have been much slower than Canada to address the issue and have not implemented as severe measures as in Canada.

So if you think it is a 10 week process in Canada, every expert I’ve read says it will be a lot longer and probably deeper in the U.S. About 70 per cent of our parts sector and about 80 per cent of our assembly sector is dependent on the U.S. So the manufacturing jobs tied to the automotive sector in Canada will take a lot longer to return than our non-manufacturing jobs. It could be the fall before we see some sense of normalcy on the manufacturing side of our sector.

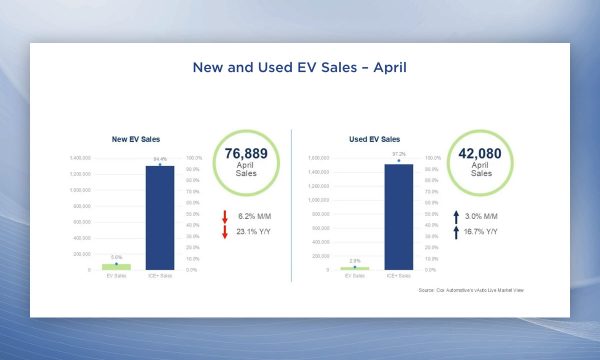

Interestingly, most dealers I’ve talked to tell me that their used vehicle department is also affected, but not nearly as bad as the new vehicle sector. I haven’t figured this out yet, but we were forecasting the used market in Canada increasing from 3.3 million to about 3.5 million this year. We now believe the used vehicle will drop a bit, but for the most part hold up fairly well compared to the new vehicle market. Dealers well positioned on the used vehicle side of the market will fare better than those who only focus on new vehicles.

And lastly, there was a fear in the sector that over this coming decade the ride-sharing and mobility services that were developing would lower vehicle ownership in North America. If there is one positive that has come from this, it is that this fear has lessened — if not abandoned.

Nobody in their right mind will give up ownership of their vehicle. We believe personal use ownership of vehicles has become much stronger as a result of this crisis. At least with your own vehicle you know who has been in it before you, which you don’t know with any of these other services.

I’ve never understood the motivation for giving up ownership of your vehicle. I accept that it might be more financially efficient. But when my great grandfather came to Canada and this was also true of my grandfather, my father and now myself — one of the top priorities in all their lives was ownership: property, housing, vehicle, recreational equipment, etc.

Indeed one of the key distinguishing features between living in Europe and moving to Canada was the definition of building a better life. Why would anyone want to give up ownership to the 1 or 2 per cent of wealthy individuals who will control these new concepts? Are we all to become serfs again?

Dennis DesRosiers is the President of DesRosiers Automotive Consultants, and one of Canada’s best known, and most sought after industry analysts.